12 ways families can review estate planning options for aging parents

Estate planning has a way of knocking only after the house is already on fire. A parent falls. A hospital form needs a signature. A bank account gets disputed. A password disappears. Someone starts opening drawers, looking for a will that nobody can find, and suddenly, love is not enough to answer the questions on the table. That is why more families are learning to talk sooner, before stress gets a vote.

AARP reported in 2024 that 93% of adults age 50 and older said it was important to have an updated legal document explaining who should receive their assets after death, yet only 51% said they had a legal will. Caring.com’s 2024 Wills and Estate Planning Study found that only 32% of Americans had a will, down 6% from 2023. That leaves many families trusting memory, goodwill, and “we’ll figure it out later” to do the job that signed documents are meant to do.

The goal is not to turn a parent’s kitchen table into a courtroom. It is to keep one hard season from becoming harder than it has to be. Health, grief, money, sibling history, old promises, and missing paperwork can collide fast when no plan exists.

The National Council on Aging’s 2026 estate planning checklist says, “Contrary to popular belief, estate planning isn’t just for wealthy people.” It matters to anyone who wants their wishes respected, their assets handled properly, and their family spared avoidable confusion.

A good review does not start with fear. It starts with care, patience, and one brave question: Do we know what Mom or Dad would want if life changed overnight?

Start With Honest, Family-Wide Conversations

Before anyone opens a folder or calls a lawyer, families need a real conversation about wishes, fears, roles, and limits.

NCOA’s estate planning guide includes discussing the plan with family or caregivers as part of its 10-step checklist, and that step matters because documents can fail emotionally if nobody understands the story behind them.

A parent may want to stay at home as long as possible, name one child as the main contact, support a charity, avoid family fights over sentimental items, or keep medical choices private until a health crisis makes privacy impossible

AARP’s 2024 data shows the gap clearly: 93% of adults 50-plus value updated estate documents, but only 51% have a legal will. The first review should sound less like an interrogation and more like protection: who should know what, where are papers stored, who should speak for you, and what would make you feel respected if you could not manage everything alone?

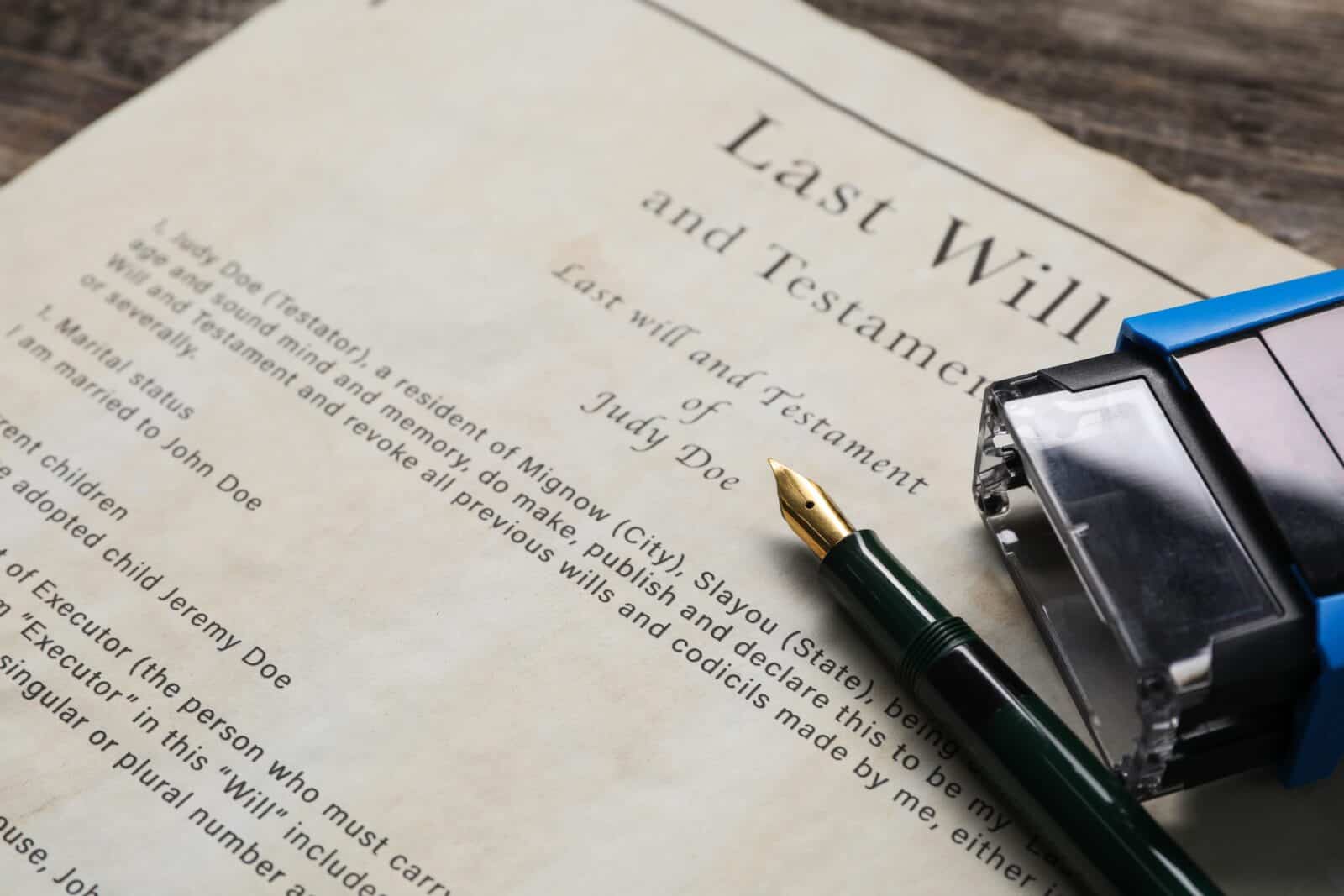

Confirm There’s an Updated Will

A will is the foundation, but an old will can be a time capsule from a life that no longer exists. NCOA says a will outlines wishes for distributing property and assets, names an executor, lists beneficiaries, and can name guardians for minor children or dependents.

Caring.com found in 2024 that only 32% of Americans had a will. AARP found that only 51% of adults age 50 and older had one, including 66% of adults 65-plus. Those numbers matter because life keeps editing the family tree: remarriage, divorce, a death, a new grandchild, a move to another state, a falling-out, or a home sale can make yesterday’s will feel like a wrong address on an important letter.

Without a valid current will, state law can decide the order of inheritance, and that result may not match a parent’s heart, promises, or family reality.

Review Durable Financial Powers of Attorney

A durable financial power of attorney is the document that families often wish they had after trouble starts. NCOA explains that a power of attorney gives an agent authority to act on someone’s behalf in certain matters, and a durable POA stays in effect even if the person loses the ability to make decisions.

NCOA’s older-adult checklist places powers of attorney as step 3, right after making a will and considering a living trust, because bills, taxes, banking, property management, and insurance do not pause when a parent becomes ill.

The review should ask practical questions: is the agent still alive, willing, trustworthy, organized, and close enough to help? Will the bank accept the document? Does it allow the agent to handle real estate, retirement accounts, taxes, and digital access? A stale POA can leave adult children stuck at the counter, holding love in their hands and lacking legal authority.

Update Healthcare Directives and Medical Proxies

Health documents can spare a family from one of the hardest forms of guessing. NCOA explains that an advance health care directive, also called a living will, states a person’s care preferences in end-of-life or emergency situations and names a health care proxy to make medical decisions in accordance with those wishes.

It can include choices about resuscitation, defibrillators, feeding tubes, pain management, and life support. NCOA also lists advance health care directives as step 4 in its older-adult estate planning checklist, which shows how closely estate planning and medical planning now sit together.

The family review should ask: who speaks to doctors, what treatments the parent wants or refuses, where the directive is stored, and whether every child knows the answer. In a hospital hallway, uncertainty can turn siblings into opponents. Clear medical instructions give grief fewer jobs to do.

Take a Full Inventory of Assets, Debts, and Key Documents

A family cannot protect what it cannot find. NCOA’s estate planning checklist tells families to gather key documents, such as property titles, insurance policies, bank accounts, and retirement accounts, and to make an inventory of assets and debts. That may sound simple, but it can save weeks of confusion later.

The list should include homes, land, vehicles, checking and savings accounts, brokerage accounts, retirement plans, pensions, life insurance, business interests, loans, credit cards, tax records, jewelry, safe deposit boxes, funeral plans, passwords, and digital accounts.

Caring.com’s 2024 study found that 40% of people without a will said they did not have enough assets to leave anyone, yet many families discover after a death that “not much” still includes accounts, sentimental items, debts, and legal obligations. A clean inventory turns scattered paper into a map. It gives the executor fewer shadows to chase.

Check Beneficiary Designations and Align Them With the Plan

One of the easiest estate planning mistakes is assuming a will controls everything. It does not. NCOA’s checklist includes naming beneficiaries for all accounts and policies, and that matters because retirement accounts, life insurance policies, transfer-on-death accounts, and some bank or brokerage accounts can pass directly to the named person.

If the beneficiary form lists an ex-spouse, a deceased sibling, an estranged relative, or no contingent beneficiary, the will may not fix it. NCOA’s 10-step list places beneficiary naming beside documents like wills, trusts, powers of attorney, and inventories, which shows how central this step is.

Families should review every IRA, 401(k), pension, annuity, life policy, and payable-on-death account, then compare those forms with the will and trust. The goal is harmony. Nothing sparks family pain like discovering that one forgotten form overruled years of spoken wishes.

Evaluate If Trusts Make Sense in 2026

Trusts are not only for families with mansions and private jets. They can help when there are blended families, special-needs beneficiaries, privacy concerns, real estate in more than one state, business interests, or a parent who wants assets managed over time.

NCOA says a living trust lets someone place assets, such as a home, bank accounts, or investments, into a trust while still using and controlling them during life, and after death, those assets go directly to chosen beneficiaries. NCOA also says a living trust can help heirs avoid probate, offer privacy, and include provisions for managing property if the person becomes incapacitated.

Its guide names marital, charitable, and special needs trusts, and notes that trusts can help maintain privacy, reduce taxes, or manage assets for children or grandchildren over time. Not every parent needs one. But the review should ask whether a simple will leaves too much exposed to delays, conflicts, public court records, or uneven family needs.

Understand 2026 Tax Rules, Exemptions, and Gifting Options

Most families will not owe federal estate tax, but tax planning still deserves a seat at the table. The IRS says the One Big Beautiful Bill Act increased the federal basic exclusion amount to $15,000,000 for calendar year 2026, and IRS inflation-adjustment guidance keeps the annual gift tax exclusion at $19,000 per recipient for 2026.

That gives high-net-worth families more room to plan gifts, trusts, and transfers, but state estate taxes, income taxes, capital gains, inherited retirement accounts, and basis rules can still shape what heirs actually receive.

Jean Bedell of Bonadio Group writes that “The most effective plans now bring income and estate tax considerations together rather than treating them as separate decisions.” That is the 2026 lesson in plain English: do not only ask who gets the asset. Ask what tax bill follows it, how liquid the estate will be, and if parents should gift, hold, sell, or place assets in trust.

Coordinate Long-Term Care, Housing, and Insurance Decisions

Estate planning is also care planning, because inheritance can disappear quickly when health needs rise. The Administration for Community Living says that someone turning 65 has a nearly 70% chance of needing some form of long-term care services and supports in their remaining years.

Women need care for an average of 3.7 years, men for 2.2 years, and 20% will need care for longer than 5 years. That makes the family review bigger than wills and bank accounts. Parents may need to discuss aging in place, assisted living, home modifications, transportation, long-term care insurance, Medicaid planning, medication management, and who will coordinate care if memory or mobility changes.

This conversation can feel tender because it touches on independence. Still, asking early is kinder than deciding during a fall, stroke, or dementia crisis. A plan for care protects more than money. It protects a parent’s voice before stress gets loud.

Watch for Financial Red Flags and Protect Against Exploitation

Estate planning should also protect aging parents from people who circle when money, loneliness, and confusion meet. The FTC’s 2024 to 2025 report estimated conservative overall fraud losses of $31.3 billion in 2024, including $10.1 billion lost by older adults, and reported that older consumers lost $159 million to tech support scams alone that year.

The FTC also said older adults reported median individual losses that were much higher than those of younger adults, with people 80 and over reporting median losses of more than $1,600. Families should watch for unusual withdrawals, unpaid bills, sudden new “helpers,” changed passwords, secretive phone calls, pressure to buy gift cards, new advisors, missing mail, or fear around finances.

Oversight should respect dignity, not treat parents like children. Trusted contacts, account alerts, read-only access, regular check-ins, and clear POA rules can help spot trouble before a lifetime of savings disappears through a screen or phone call.

Align Charitable Giving and Legacy Wishes With the Plan

Some parents want their estate to say something about who they were, not just what they owned. NCOA lists charitable trusts as one tool that can support a cause while still providing for family, and Bonadio Group notes that families are using trusts in 2026 to coordinate charitable goals, manage ongoing tax exposure, and prepare for long-term business transitions.

This is where a review can move from paperwork to legacy. Does a parent want to support a church, school, shelter, scholarship fund, medical charity, or local arts group? Should gifts come through a will, trust, beneficiary designation, donor-advised fund, qualified charitable distribution from an IRA, or direct lifetime giving?

The details matter because a vague promise can fade, and heirs may remember wishes differently. Writing down charitable intent turns memory into action. It also helps families balance generosity with taxes, liquidity, and the needs of surviving spouses or dependents.

Make Estate Reviews Ongoing

A good estate plan is not a dusty binder that gets one signature and then sleeps for 15 years. NCOA says an estate plan should not be “one and done,” and recommends a review every 3 to 5 years or after major changes, such as marriage, divorce, birth, death, or a move to another state.

Russo Law Group’s 2026 guidance says, “In 2026, the most effective estate plans are reviewed regularly—not reactively.” That line captures the whole point. Families change. Tax rules shift. Parents move. A trusted agent may become ill. A beneficiary may die. A grandchild may need support. A home may be sold. Digital assets may grow.

Estate planning works best as a living review, not a last-minute scramble. Put a reminder on the calendar, gather the documents, ask what changed, and update the plan while everyone can still speak clearly for themselves.

A Short Reflective Close

Estate planning is love with instructions attached. It does not remove grief, and it cannot make aging simple. But it can remove some of the confusion that grief should not have to carry. AARP found that 93% of adults age 50 and older value updated legal documents for passing assets, yet only 51% have a legal will.

NCOA’s checklist shows the work is manageable when families take it step by step: make a will, consider a trust, create powers of attorney, prepare health directives, gather documents, name beneficiaries, list assets and debts, write down memorial wishes, store papers safely, and talk with family. That is not cold. That is care, written down before the storm.

Key Takeaways

Families should start estate planning conversations before a health crisis forces them. AARP found that 93% of adults age 50 and older say updated asset-transfer documents matter, but only 51% have a legal will, while Caring.com found only 32% of U.S. adults had a will in 2024.

Core documents include a will, financial and health care powers of attorney, an advance health care directive, beneficiary forms, and an inventory of assets and debts. NCOA’s 10-step estate planning checklist places all of these inside a practical plan that families can update over time.

The 2026 tax rules create planning room for wealthier families, with the IRS setting the federal basic exclusion amount at $15,000,000 and the annual gift tax exclusion at $19,000 per recipient. Tax planning still needs a professional review because state and federal taxes, capital gains, and retirement accounts can affect the final outcome.

Estate planning should also cover long-term care, fraud protection, charitable wishes, and regular updates. The FTC estimated that older adults lost $10.1 billion to fraud in 2024, and NCOA recommends reviewing estate plans every 3 to 5 years or after major life changes.

Disclaimer – This list is solely the author’s opinion based on research and publicly available information. It is not intended to be professional advice.

Like our content? Be sure to follow us