13 myths keeping the middle class trapped financially

Economists warn that shrinking middle-income demographics and rising living costs are making upward mobility harder for many American families.

The middle class in the United States faces structural financial challenges that make long-term upward mobility increasingly difficult. Many households earning historically stable wages find that their monthly net income does not allow them to accumulate substantial personal wealth. This financial stagnation often persists despite consistent workplace effort and a commitment to conventional economic practices.

Sociologists and economists document this trend by tracking changes in the distribution of household income across the population.

Only about 51% of American adults now reside in middle-income households, according to a Pew Research Center analysis of government data, down from a much larger share in previous decades. Overcoming this structural ceiling requires a realistic evaluation of traditional behavioral patterns that frequently limit family savings.

Viewing A Home As An Investment

The deeply ingrained cultural belief that a primary residence functions as a lucrative investment drives families to overspend on real estate transactions. Homeowners calculate their net worth by subtracting their outstanding mortgage balance from the structure’s current estimated market value.

A primary residence is a consumption asset that requires ongoing cash outflows for maintenance, insurance, and structural repairs. True investments provide direct cash inflows to the owner regularly rather than consuming operational capital.

Relying entirely on localized property appreciation ignores the significant transaction fees and moving expenses involved in liquidating real estate wealth.

The Safety Of A Steady Paycheck

Relying entirely on a single corporate salary is often considered the most reliable way to ensure lifelong household stability. Traditional career guidance emphasizes that securing a full-time position with standard institutional benefits represents the definitive endpoint of personal financial planning.

True wealth accumulation rarely occurs when an individual relies exclusively on trading finite working hours for a fixed corporate wage.

Over the last several decades, wage growth for typical workers has often lagged behind productivity gains and the rising cost of living, eroding purchasing power even as salaries slowly increase. Developing independent revenue streams or private investments is what separates long-term solvency from permanent financial stagnation.

Financing A Brand New Vehicle

Purchasing a factory-fresh automobile is a common milestone that many individuals use to signal their entry into economic comfort. Dealership finance departments make these transactions highly accessible by extending repayment terms over six or seven years to minimize the immediate monthly impact.

Consumers frequently focus entirely on matching that fixed monthly obligation to their current payroll cycle without calculating the total long-term interest cost. Vehicles lose a significant percentage of their market value during the initial years of ownership, draining household capital through rapid depreciation.

Official consumer liability tracking shows that auto loan balances in the United States have climbed to well over a trillion dollars, creating a sizable fixed burden on family cash flow. Allocating substantial monthly funds to a depreciating mechanical asset leaves households with very little capital remaining for investment.

Purchasing The Maximum Allowed Home

Underwriters utilize rigid mathematical formulas to calculate the absolute largest mortgage loan a household can qualify to receive based on gross income. Many buyers interpret this maximum pre-approval figure as an official endorsement to purchase the most expensive property within their reach.

This structural assumption overlooks the ancillary expenses of property ownership, including local property taxes, neighborhood association assessments, and structural maintenance. Stretching a household budget to the absolute limit leaves no financial margin for unexpected job losses or sudden medical developments.

The Myth Of Good Debt

Conventional financial guidance frequently separates liabilities into negative categories, such as retail store accounts, and positive categories, such as educational loans. This framework leads well-meaning individuals to believe that borrowing large sums for higher education or residential real estate is always an intelligent choice.

Debt is a direct drain on net household income, regardless of the structural label on the monthly billing statement.

The Federal student loan balances total well over $1 trillion, contributing to delays in homebuying, family formation, and other milestones for many borrowers. Carrying high debt balances forces families to redirect significant portions of their earnings to institutional lenders rather than building personal wealth.

Relying On Credit Card Rewards

Financial institutions launch expansive marketing campaigns promoting cash-back points and complimentary travel miles to encourage consumers to utilize credit for daily transactions. Consumers often adopt the habit of executing every purchase with plastic, believing they are maximizing their personal returns at the expense of the banking system.

This optimization strategy fails when a household carries a rolling monthly balance, triggering high double-digit interest penalties. Federal Reserve data show that the average interest rate on interest-charging credit cards recently climbed above 20%.

This makes any unpaid balance extremely expensive over time. Attempting to collect a modest promotional reward while paying very high interest represents a negative mathematical equation.

Saving Your Way To Wealth

Traditional advice posits that placing cash into a standard brick-and-mortar depository account is the definitive foundation of personal security. Families diligently transfer small percentages of their weekly earnings into these vehicles, expecting the accumulated balance to fund their eventual retirement.

Traditional savings instruments rarely offer interest yields that keep pace with the real-world inflation rate of consumer goods. In recent years, average savings account rates have often remained near historical lows while inflation periodically spiked higher.

Leaving large quantities of currency idle means the purchasing power of that capital erodes year after year, which is why true independence requires a shift from passive capital preservation to active asset deployment.

The Ultimate Goal Of Retirement

The standard professional trajectory promises that forty years of continuous workplace labor will grant entry into a secure period of total leisure. Employees spend decades focusing on age sixty-five, treating it as the official finish line of their mandatory participation in the labor force.

This cultural structure encourages individuals to defer their personal freedom and experiential goals until the final chapters of life. Relying completely on corporate pensions or shifting public social security funding leaves aging workers exposed to legislative changes.

Official projections from the Social Security Administration have repeatedly warned that, without adjustments, future benefits may need to be reduced relative to currently scheduled levels. True financial stability requires achieving functional independence during your peak working years rather than targeting an arbitrary chronological age milestone.

Waiting For The Perfect Investment Time

Many analytical households remain entirely on the sidelines of major equity markets, waiting for an ideal economic entry point. They review conflicting financial media reports regarding market volatility and choose to hold their cash reserves until conditions appear entirely predictable.

Waiting for absolute economic certainty results in missing out on the compounding growth that occurs over extended periods of market participation. Historical analyses of major stock indexes show that being out of the market during just a small handful of the best-performing days can dramatically reduce long-run returns.

Committing capital to diversified markets on a consistent schedule is far more critical than attempting to predict cyclical market bottoms.

The Prestige Of Elite Higher Education

Parents frequently liquidate their personal retirement assets or take on additional liabilities to send their children to private universities with high tuition costs. They believe that a credential from an elite institution functions as a guaranteed passport into high-paying professional employment sectors.

This emotional decision often saddles both the older generation and the entering professional with six-figure debt obligations. The modern employment market places an increasing premium on demonstrable technical competencies and practical execution rather than institutional branding.

Employer surveys have found that skills and relevant experience often rank above school name when hiring decisions are made. Starting a professional career with an immense debt burden restricts a young worker’s ability to take calculated entrepreneurial risks or invest early.

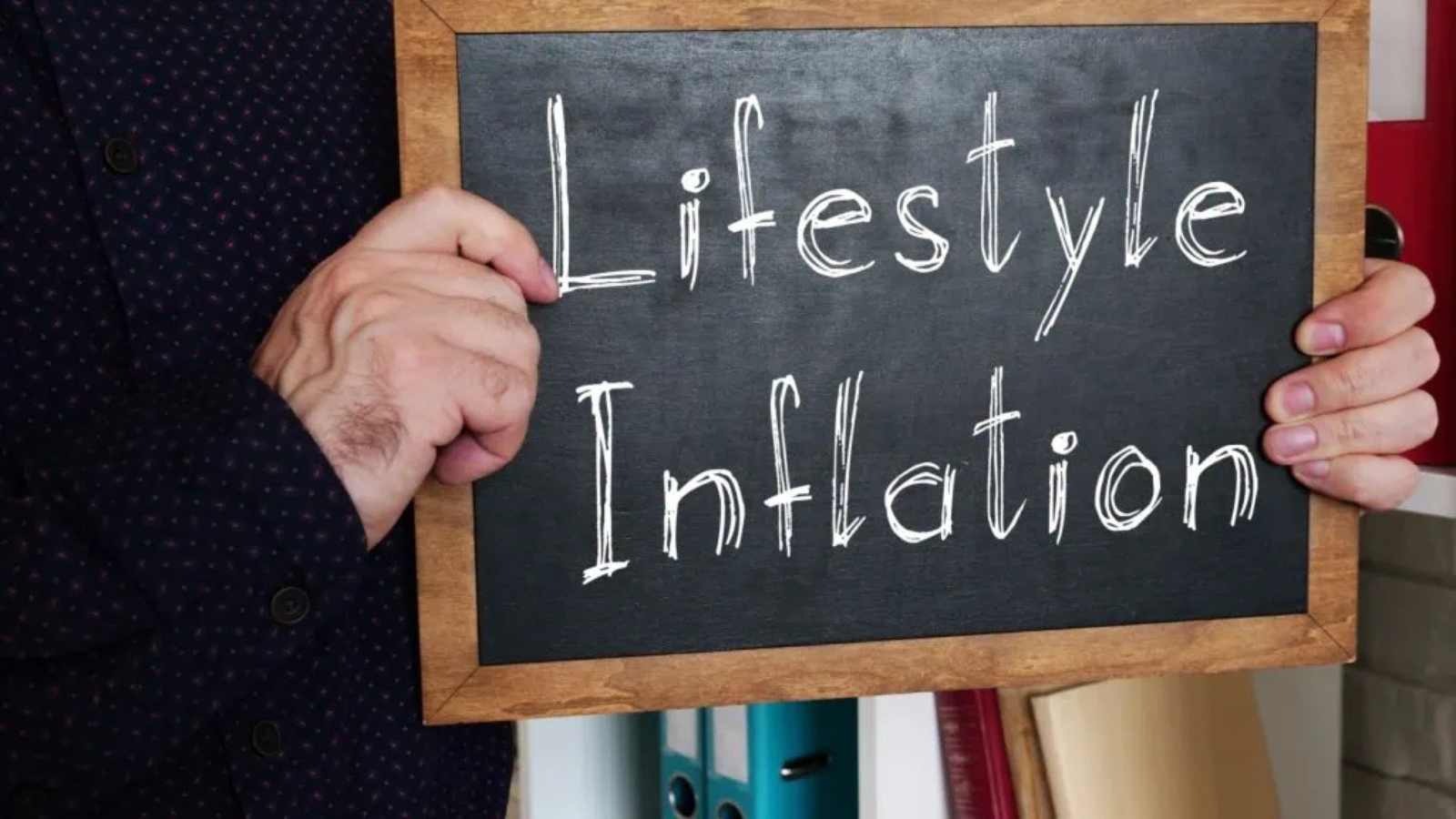

Upgrading Lifestyle With Every Raise

When a salaried professional receives an advancement, the immediate behavioral response is often to increase personal consumption habits. A higher base salary quickly translates into a more expensive residential lease, premium consumer electronics, and upscale dining experiences.

This consumption pattern keeps working families trapped on a treadmill where their fixed expenditures rise in perfect lockstep with their earnings. True capital accumulation requires maintaining a stable standard of living even as personal compensation increases significantly over time.

Relying Entirely On Public Assistance

Many middle-income earners assume that state-sponsored social safety programs and employer-provided health insurance options will fully protect them during an emergency. They review their standard payroll deductions and assume that these public mechanisms will eliminate all financial risk during a personal crisis.

This passive approach prevents individuals from taking personal responsibility for establishing independent cash reserves. Public safety networks face structural funding long-term challenges and are rarely designed to replace a worker’s full net income during an extended disruption.

Depending exclusively on external institutions means surrendering control of your personal security to shifting legislative priorities. Establishing a private emergency fund provides the only reliable defense against sudden institutional adjustments.

The Illusion Of High Income Wealth

Observing a high annual salary figure on a tax document can easily create the false impression of absolute financial success. Professionals earning six-figure incomes often classify themselves as wealthy while ignoring the negative reality of their actual net worth statements.

True wealth is measured by the duration of time a household can sustain its current expenses if all primary employment salary streams stop immediately. High earnings accompanied by high fixed overhead simply create a dependency loop that requires continuous labor to maintain.

Key Takeaway

Breaking free from these financial limitations requires an intentional reevaluation of daily consumption habits and long-term asset accumulation strategies. Genuine stability is never achieved by projecting an aura of success through high-end consumer goods, premium vehicles, or maximum-sized mortgages.

It demands a conscious choice to live significantly below your current earning capacity, invest capital consistently, and treat incoming revenue as a tool for acquiring cash-flowing assets rather than collecting consumer receipts.

Disclaimer – This list is solely the author’s opinion based on research and publicly available information. It is not intended to be professional advice.

Like our content? Be sure to follow us