11 ways America’s housing rules are failing ordinary people

America’s housing system is quietly stacking the deck against ordinary people. The rules (zoning codes, mortgage underwriting, federal caps, and local regulations) make scarcity a constant. Mortgages are climbing past $2,000 a month, home prices have more than doubled since the ’80s, while incomes lag behind, and three‑quarters of households can’t touch a median‑priced home.

Millions of families are paying more than half their income on rent, older adults are trapped in unsuitable homes, and low-income renters often face eviction as a routine threat. This isn’t a temporary glitch. It’s a system engineered to favor wealth, maintain inequality, and keep opportunity out of reach for those who need it most.

The American Dream now costs more than most households will ever earn

Affordable housing is vanishing while costs soar. The U.S. faces a shortage of more than seven million affordable homes for over ten million extremely low-income renters, leaving just 33 homes for every 100 families who need them.

About 70% of these renters pay more than half their income on rent, forcing trade-offs between shelter, food, and healthcare. Mortgage payments have climbed from under 20% of income pre-pandemic to over 30% today, and Goldman Sachs estimates three to four million additional homes are needed just to close the supply gap. The result is a nationwide affordability crisis baked into policy.

Zoning laws literally outlaw affordable housing

Across much of the country, local zoning codes reserve land almost exclusively for detached single-family homes. In some cities, up to 75% of residential land bans duplexes, triplexes, or apartments, pricing out lower-income families near jobs and transit.

Minimum lot sizes, setbacks, and parking requirements inflate land use per home, driving up prices by as much as 40% over a decade in some communities. Experts at Goldman Sachs call restrictive land-use rules the largest barrier to closing the supply gap, and the result is clear: NIMBY rules lock out affordable housing before the first shovel hits the ground.

A 1990s law froze public housing while rents exploded

Federal rules like the Faircloth Amendment prevent HUD from funding net new public housing above 1999 levels. Even as waiting lists grow and units age into disrepair, the law legally bars adding new deeply affordable units, leaving millions with few options.

Combined with decades of disinvestment, this cap reinforces scarcity at the federal level, making it nearly impossible for low-income renters to escape the cycle of high rent, poor-quality housing, and limited upward mobility. The system ensures that public housing serves only as a static safety net, rather than a pathway to stability.

The mortgage system still favors White wealth

Homeownership remains structurally unequal. Non-Hispanic White Americans consistently achieve higher homeownership rates than Black and Hispanic households, who face higher mortgage denial rates; over 15% compared to about 8% overall.

Combined with higher rent burdens, lower savings, and concentrated job access, these disparities mean low-income and minority families are disproportionately blocked from building wealth through housing. Even “race-neutral” policies continue to reproduce generational inequity, highlighting that access to the American Dream is still filtered through historic and structural barriers.

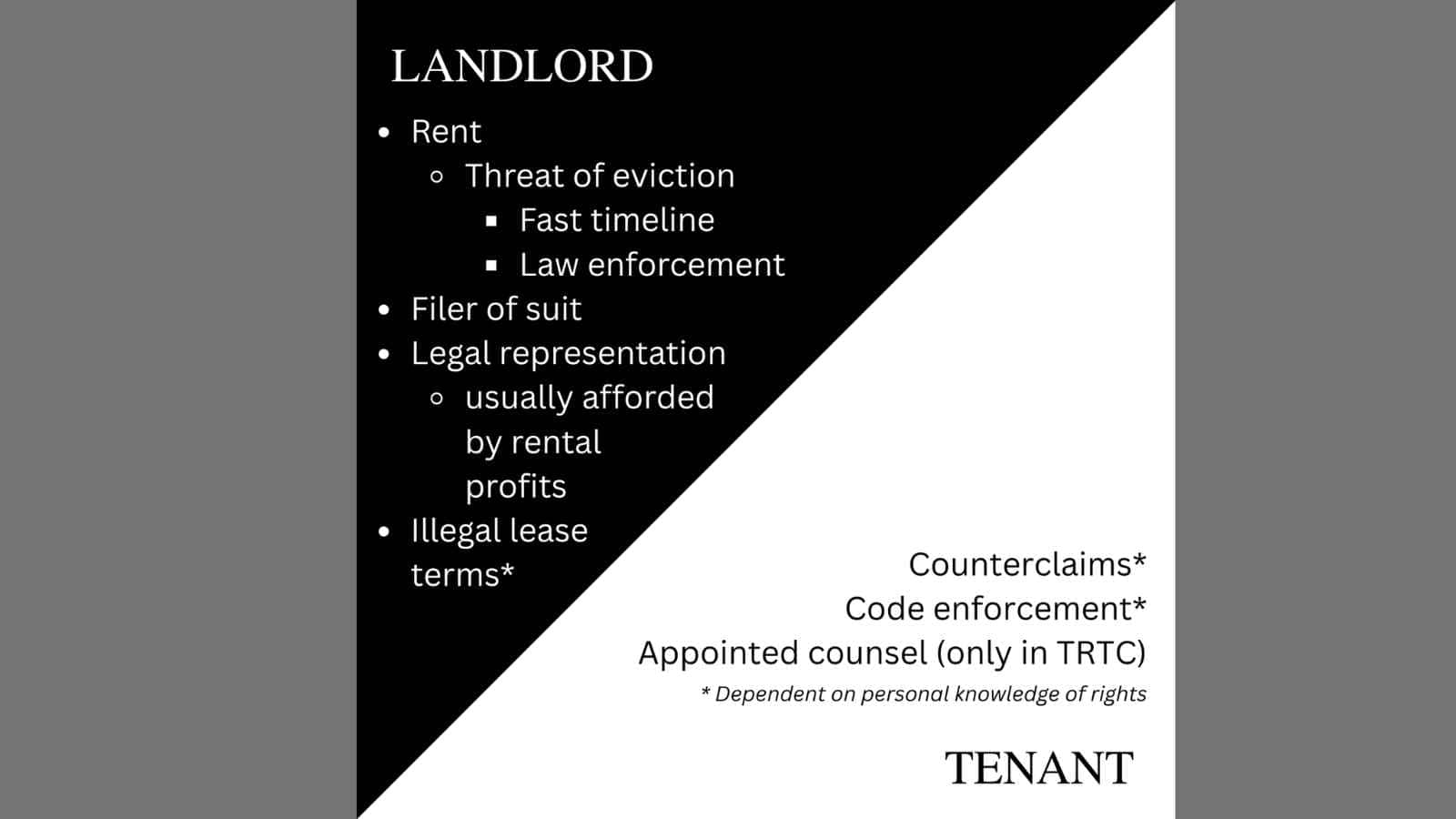

Landlords can file an eviction as cheaply as a late-fee notice

Eviction is routine, not rare. Roughly 2.7 million renter households face eviction threats annually, and filing costs for landlords are minimal, often just a few months’ rent. The Eviction Lab reports that about 7.9% of households in monitored areas received eviction filings in 2025, meaning one in thirteen families is at risk each year.

For low-income tenants, who often lack savings or legal support, an eviction can be catastrophic—disrupting work, schooling, and health while reinforcing cycles of instability. Policy and court structures make this a predictable, even normalized, outcome.

Younger buyers are locked out by mortgage rules

The median new-home price in the U.S. has climbed to nearly $496,000, with mortgage rates hovering above 6%, creating a “lock-in” where existing owners stay put, and new buyers struggle to enter the market. Underwriting rules favor perfect credit, W‑2 income, and large down payments, shutting out renters with student loans, gig work, or limited family wealth.

Nearly half of all U.S. households cannot afford even a $250,000 home under current conditions. For millions, these rules mean that despite the desire to buy, the system effectively bars them from participating in homeownership at all.

Local rules block building even when demand is obvious

Construction remains below demand, and local planning codes make recovery painfully slow. Population growth continues, yet sales of existing homes hover around 4 million annually, near post-2008 lows. Zoning bottlenecks, minimum lot sizes, and parking mandates further constrain supply, while permitting processes drag out projects for years.

Analysts at Brookings and the Cato Institute note that even when developers want to build, local “rulebooks” act as invisible walls, keeping affordable units out of high-demand neighborhoods and worsening both scarcity and prices.

Older adults are trapped in homes that no longer fit

Aging Americans face their own housing squeeze. Many seniors want to downsize or move closer to services, but affordable, accessible units near transit or healthcare are scarce.

Urban Institute research highlights that the same shortages and zoning rules limiting supply for younger families also block aging populations, leaving some seniors in unsafe, isolating, or cost-burdened living situations. The housing system was designed for a young nuclear family in a detached house, not for older adults seeking flexibility or community support.

Housing assistance is rationed by policy, not by need

Even when households qualify for federal help, access is limited. Only one in four extremely low-income families receives assistance through programs like Housing Choice Vouchers or the Housing Trust Fund.

Long waiting lists, underfunded programs, and deep subsidy requirements mean that millions go without support, leaving the most vulnerable to face soaring rents, eviction risk, and unstable housing. The system turns entitlement into a lottery, and eligibility does not guarantee shelter.

Chronic rent burden punishes low-income families

Extreme rent-to-income ratios are baked into the system. For extremely low-income households, only 33 affordable rental units exist for every 100 households, forcing 70% to spend over half their income on rent. These households sacrifice food, healthcare, transportation, and educational opportunities just to keep a roof overhead.

This “permanent rent shock” is no accident. It reflects policies and market structures that tolerate extreme cost burdens rather than prevent them, leaving families in a continuous state of financial insecurity.

Housing rules hardwire inequality and segregation

Zoning and land-use laws concentrate wealth and opportunity in certain neighborhoods while excluding lower-income and minority families. Research shows that restrictive single-family zoning raises prices, limits rentals, and perpetuates racial and economic segregation.

Low-income and minority households are often forced to live farther from good schools, jobs, and transit, reinforcing cycles of inequality. The rules don’t just fail individual households; they structure American life in a way that entrenches privilege and limits mobility for generations.

Disclaimer – This list is solely the author’s opinion based on research and publicly available information. It is not intended to be professional advice.

Like our content? Be sure to follow us